Views: 20

Universal Audit Data Converter (UADC)

- 1. Overview

- 2. Developments in Audit Data Standards

- 3. Role of UADC

- 4. Improvements in Auditing with UADC

- 5. Generic Data Conversion Processing

- 6. Syntax Binding

- 7. Semantic Binding

- 8. Advantages of Adopting xBRL-CSV

- 9. Liberation from Vendor Dependence

- 10. Long-Term Data Storage Issues

- 11. Accounting Data Standard Interface

Presentation notes are available at:

https://www.sambuichi.jp/wu_wei/index.html?note=/2023/11/dfda6aee-7c62-4e7a-88fc-055c8e2283fc

Nobuyuki SAMBUICHI

ISO/TC295 Audit data services

Convener at SG1 Semantic model

Co-project leader at ISO/AWI 21926 Semantic data model for audit data services

1. Overview

Standardization of audit data is essential for a transparent and efficient audit process. Significant developments in this field include the AICPA’s “Audit Data Standard” and China’s GB/T 24589. These standards aim to enhance the quality and consistency of audit data. The AICPA’s Audit Data Standard[1] provides standards for data auditing, and China’s GB/T 24589 mandates data collection from all domestic accounting software and analysis by regulatory agencies. ISO/TC 295 Audit data services[2] established ISO 21378:2019 Audit data collection[3].

The Universal Audit Data Converter (UADC) corresponds to these standardized data formats, converting and integrating various formats of audit data into a unified standard format, facilitating rapid and efficient analysis and auditing.

UADC also streamlines and standardizes the conversion of audit data between various data formats such as CSV, XML, JSON, through its generic data conversion processing. It extends the syntax binding defined in European Standard EN 16931 and enables data conversion based on corresponding definitions, realizing the Japanese version of the Core Invoice Gateway. In semantic binding, it maps flat CSV columns to the hierarchical semantic definition elements of data, maintaining each corresponding definition for flexible adaptation to software upgrades and system changes.

UADC adopts xBRL-CSV as its standard CSV format, allowing effective representation of data with hierarchical structures in a single file. This reduces JOIN operations and administrative burdens in relational databases, simplifying and speeding up data processing.

Furthermore, UADC frees users from the constraints of specific vendors and platforms, solving long-term data storage issues. This allows companies to utilize past data in line with current business needs, improving data management efficiency and reducing risk.

2. Developments in Audit Data Standards

2.1. Importance of Audit Data Standardization

Standardization of audit data is crucial for achieving efficient and transparent audit processes. Key developments in this field include the Audit Data Standard released by AICPA in 2015 and the accounting data collection standard GB/T 24589 Financial Information Technology ─ Data Interface of Accounting Software by China SAC/TC 341 in 2010. These standards aim to enhance the consistency and quality of audit data.

2.2. AICPA’s Audit Data Standard

AICPA’s Audit Data Standard provides standards for the collection and reporting of audit data, supporting data audits. ISO 21378:2019 is greatly influenced by the expertise provided by ANSI in the USA for AICPA’s ADS.

2.3. China’s GB/T 24589

China’s GB/T 24589 enables integrated collection of accounting data at the China National Audit Office and annual accounting detailed data analysis at data centers, contributing to the efficiency of audit processes.

2.4. ISO/TC 295 Audit data services

Based on these backgrounds, ISO/TC 295 Audit data services was established in 2015 as a PC (Project Committee) on China SAC’s proposal and formulated ISO 21378:2019 Audit data collection. In 2021, Study Group 1 Semantic model started its investigation under ISO/TC 295. From 2022 to 2023, demonstration projects (POCs) such as the development of the Core Invoice Gateway and a specialized browser for journal entry information were conducted with the cooperation of XBRL Japan. These projects aim to further strengthen the methodology of collecting, converting, and analyzing audit data, aiming for further efficiency in the audit process. UADC was developed against this background of POC. From 2023, based on the proposal of SG1, the formulation of the semantic model standard specification in ISO/AWI 21926footnote:[Semantic data model for audit data services https://www.iso.org/standard/

86895.html] has started.

3. Role of UADC

Using UADC enables the conversion and integration of audit data of various formats into a unified standard format, making data analysis and auditing more rapid and efficient.

3.1. Application to ESG Report Auditing

The role of UADC is particularly important in the auditing of Environmental, Social, and Governance (ESG) reports. Raw data from manufacturing equipment and factory control computers often have proprietary formats and are challenging to output in standard formats. By using UADC, this raw data can be converted into a unified data format, providing consistent information needed for auditing ESG reports. This improves the accuracy and transparency of ESG reporting, providing more reliable information to stakeholders.

4. Improvements in Auditing with UADC

4.1. Efficiency and Speed

Audited companies can quickly respond to accounting audits using detailed data without spending time conforming to specific data formats required by audit authorities or firms. This not only saves time in the audit process but also opens the way to deeper analysis and more accurate audit results.

4.2. Consistency and Quality Improvement

Using standardized data formats maintains the quality and consistency of data, enhancing the reliability of audit results. The ability to convert data from different systems and formats into a unified format makes it easier to integrate data from various sources.

4.3. Summary

The conversion and standardization of audit data by UADC provide significant value in accounting audits and ESG report auditing. Audited companies can achieve quicker and more efficient audit processes, further enhancing the quality and transparency of ESG reporting. This improves the quality and speed of auditing and data analysis, providing more valuable insights for companies.

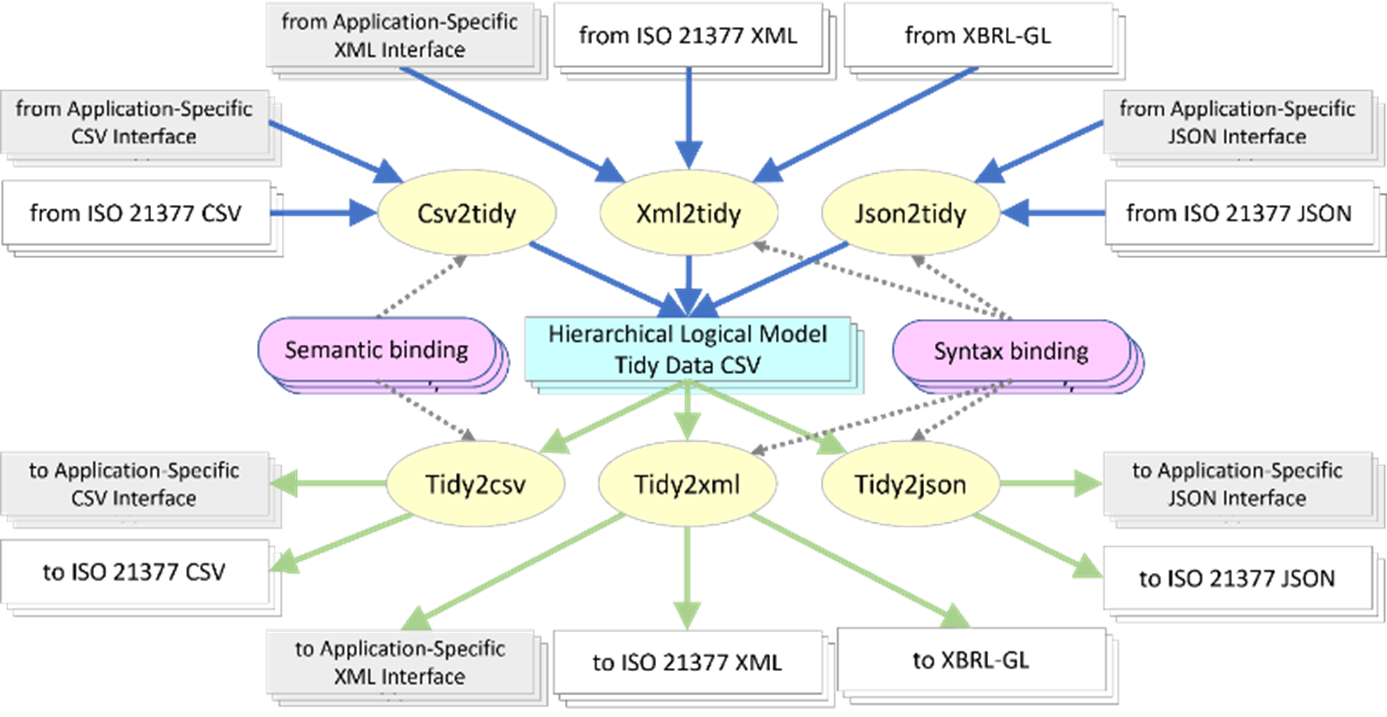

5. Generic Data Conversion Processing

UADC’s generic data conversion processing was developed to streamline and standardize the maintenance and development of data conversion programs that required modifications for new formats each time the source or target interface format changed. By specifying the destination of XML elements using XPath and our proprietary semantic path definitions for CSV columns, we have generalized the program coding for conversion processing. This targets various data formats such as CSV, XML, JSON.

6. Syntax Binding

UADC’s syntax binding is a crucial function that enables consistent conversion of audit data between different data formats. In particular, in the European Standard EN16931 (standard for electronic invoicing based on VAT regulations), the concept of syntax binding is defined by CEN/TS 16931-3. This clearly defines the correspondence between Core Invoice Usage Specification (CIUS) and the XML schema syntax of UBL 2.1 and UN/CEFACT CII D16B.

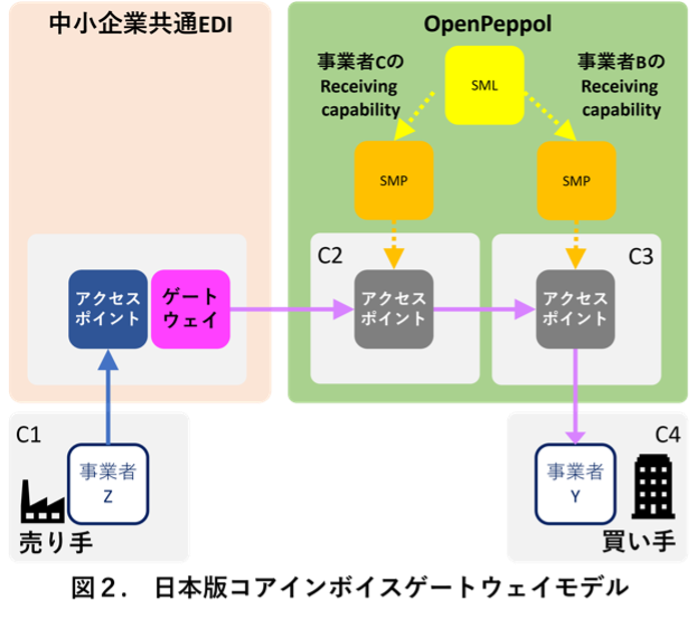

6.1. Japanese Core Invoice Gateway

In the Japanese Core Invoice Gateway, we have refined the concept of syntax binding defined in EN16931 by introducing XPath. This allows the mutual conversion of electronic invoices (JP PINT) defined using UBL 2.1 in Open Peppol and those compliant with UN/CEFACT CII for SME common EDI according to binding definitions. In the development process, we developed a new logical model for the Japanese Core Invoice and defined syntax binding with it.

Program page:

https://www.sambuichi.jp/core-japan/

6.2. XBRL Taxonomy

In the Japanese Core Invoice Gateway, we have registered the syntax binding in the XBRL taxonomy and used xBRL-CSV files as intermediary files. The data conversion of JP PINT to standard CSV and standard CSV to common EDI electronic invoices is performed by a generic Java conversion program.

6.3. Adapting to System Changes

With such a configuration, even if the interface definitions of the source and destination change, it is possible to respond by limiting to changes in the syntax binding definitions, without requiring modifications to the data conversion program. This improves the flexibility and sustainability of the data management process, contributing to the efficiency of audit operations.

7. Semantic Binding

7.1. Its Role

Although the input and output of CSV files have been easily programmable and thus not considered much of a problem, there have often been many cases where it was questionable whether the content of these processes was clearly documented as specifications, leading to difficulties in maintenance. Semantic binding significantly reduces the burden of program maintenance by defining the mapping of transformation processes as a correspondence dictionary within the taxonomy definition.

Semantic binding in UADC (Uniform Audit Data Collection) is very important for maintaining semantic consistency of data. In this process, data is distributed according to the definition of semantic hierarchies, such as mapping specific CSV columns to auxiliary account codes like cost department codes or supplier codes.

7.2. Flexibility and Adaptability

This approach is flexible and can adapt when the format of the CSV interface changes due to app version updates or when migrating to different software. By changing the semantic binding to the altered interface format and registering it with the XBRL taxonomy, it is possible to respond quickly without waiting for program modifications. This maintains the continuity and consistency of the data management process, improving the efficiency of audit work.

7.3. Contributing to Efficiency and Speed

Semantic binding in UADC significantly streamlines the data conversion process for auditing. It facilitates data migration between different software systems, maintaining data integrity and accuracy. Particularly in the fields of auditing and data analysis, this directly translates into saving time and resources, supporting quicker and more accurate decision-making.

7.4. Wickham’s Tidy Data Concept

According to Wickham’s definition of Tidy Data, data should be organized as follows:

– Each variable forms a column: Each variable (measurement or attribute) in the dataset has its own column.

– Each observation forms a row: Each row represents a single observation.

– Each type of observational unit forms a table: Different observational units are placed in separate tables.

Related Article:

https://www.sambuichi.jp/?cat=68

Wickham’s Paper:

https://www.jstatsoft.org/article/view/v059i10

7.5. xBRL-CSV and Hierarchical Tidy Data

xBRL-CSV extends the concept of Wickham’s Tidy Data, particularly in handling hierarchical data, with features such as:

– Support for hierarchical data structures: While Tidy Data originally assumes a flat data structure, xBRL-CSV supports hierarchical data structures, allowing more efficient representation of naturally hierarchical data like complex organizational data or accounting data.

– Expression of multi-level variable relationships: xBRL-CSV allows for associating multiple levels of variables within a single record, enabling the representation of accounting information related to a specific transaction and related departmental information in one integrated view.

– Extensibility and flexibility: xBRL-CSV is based on the XBRL taxonomy, making it easily extendable and customizable to existing accounting standards and reporting requirements.

7.6. In the Case of Journal Entry Information

For observational units of journal entries, xBRL-CSV enables hierarchical data representation as follows:

– Information per entry: Each row represents observations like posting date, entry date, and description for each entry.

– Detail line information: Details like amounts for each account and applicable consumption tax are recorded in line items.

– Detailed information per auxiliary account: Detailed information for auxiliary accounts defined in accounts, like bank accounts, suppliers, cost departments, are registered as row observations using the same auxiliary account number and name fields.

– Hierarchical recording: These hierarchies can be recorded in a single file, providing great convenience in data organization and analysis.

Journal Entry Information Dedicated Browser

https://www.sambuichi.jp/core-japan/journal_entry/

8. Advantages of Adopting xBRL-CSV

In UADC, xBRL-CSV is adopted as the standard CSV format. This allows data with hierarchical structures typically seen in XML or JSON to be effectively represented in a single CSV file.

8.1. Reduction in JOIN Operations

In typical relational databases (RDB), JOIN operations are needed to combine related data across multiple tables. However, with the adoption of xBRL-CSV, related data can be hierarchically managed within a single file, eliminating the need for these complex JOIN operations.

8.2. No Need for Database Maintenance

Maintaining a relational database involves many tasks, such as ensuring data integrity, security, and backup. However, using xBRL-CSV eliminates the need for these complex database management tasks, significantly reducing the administrative burden.

8.3. Simplification and Speeding Up of Program Processing

Using xBRL-CSV simplifies and speeds up data processing. Since the data is contained within a single file, data reading and writing are performed efficiently, improving the overall speed of data processing.

8.4. Summary

The adoption of xBRL-CSV in UADC greatly contributes to the efficiency of data processing. It allows hierarchical data, like those in XML or JSON, to be represented in a single file, eliminating the need for complex JOIN operations. These extensions maintain the basic principles of Wickham’s Tidy Data while catering to

modern business and accounting needs for more complex and hierarchical data structures. This makes data analysis, interpretation, and reporting easier, supporting organizational decision-making processes. It also realizes the reduction of the administrative burden of relational database management and the simplification and acceleration of data processing, making data management and analysis more efficient and faster for businesses.

9. Liberation from Vendor Dependence

One of the key features of UADC is its ability to free users from the constraints of specific software vendors or platforms. This allows businesses to have more flexibility in managing and converting audit data.

For example, suppose a company uses a specific ERP (Enterprise Resource Planning) system. This system may have its proprietary data format, limiting compatibility with other systems or applications. In such cases, converting data to other formats may require dependence on specific vendor tools or services, potentially increasing costs and decreasing efficiency in data conversion.

By adopting UADC, this company can easily convert data output from the ERP system from its proprietary format to standard format CSV, and then to purpose-specific CSV, XML, or JSON formats. This facilitates data integration with other systems and applications, allowing data analysis and report generation without dependence on vendor-specific tools.

9.1. Effects

-

Cost Reduction: Independence from specific vendor tools and services reduces license fees and support costs.

-

Increased Efficiency: Data conversion and integration between different systems become quicker and easier.

-

Enhanced Flexibility: Lower barriers to adopting new systems or applications, allowing flexible response to business expansion or changes.

9.2. Summary

The liberation from vendor dependence through UADC supports business growth and innovation by enabling companies to manage audit data more effectively and choose appropriate tools and services for various business needs.

10. Long-Term Data Storage Issues

UADC addresses the problems of legacy systems, i.e., outdated software or data management systems. Companies can easily access past data and integrate it with contemporary systems.

For example, consider a company that has stored data in an old accounting software. This software may not be compatible with current data standards or formats, making it difficult to use past financial data with new systems or applications. As a result, to access past data, it becomes necessary to maintain the old system, imposing a burden on the company in terms of both cost and effort.

By implementing UADC, the company can convert data output from the old accounting software into modern data formats. Even without old systems, data in old formats can be converted to standard CSV or XML formats and integrated with current accounting systems or analysis tools.

10.1. Effects

-

Improved Data Access: Past data becomes easily usable in new systems, enhancing data utility.

-

Cost Reduction: Reduces the cost of maintaining old systems, allowing a transition to efficient data management.

-

Enhanced Risk Management: Improved data compatibility reduces the risk of data loss or access issues.

10.2. Summary

UADC’s solution to long-term data storage issues enables the use of past data according to contemporary business needs, significantly contributing to the efficiency of data management and risk reduction for companies.

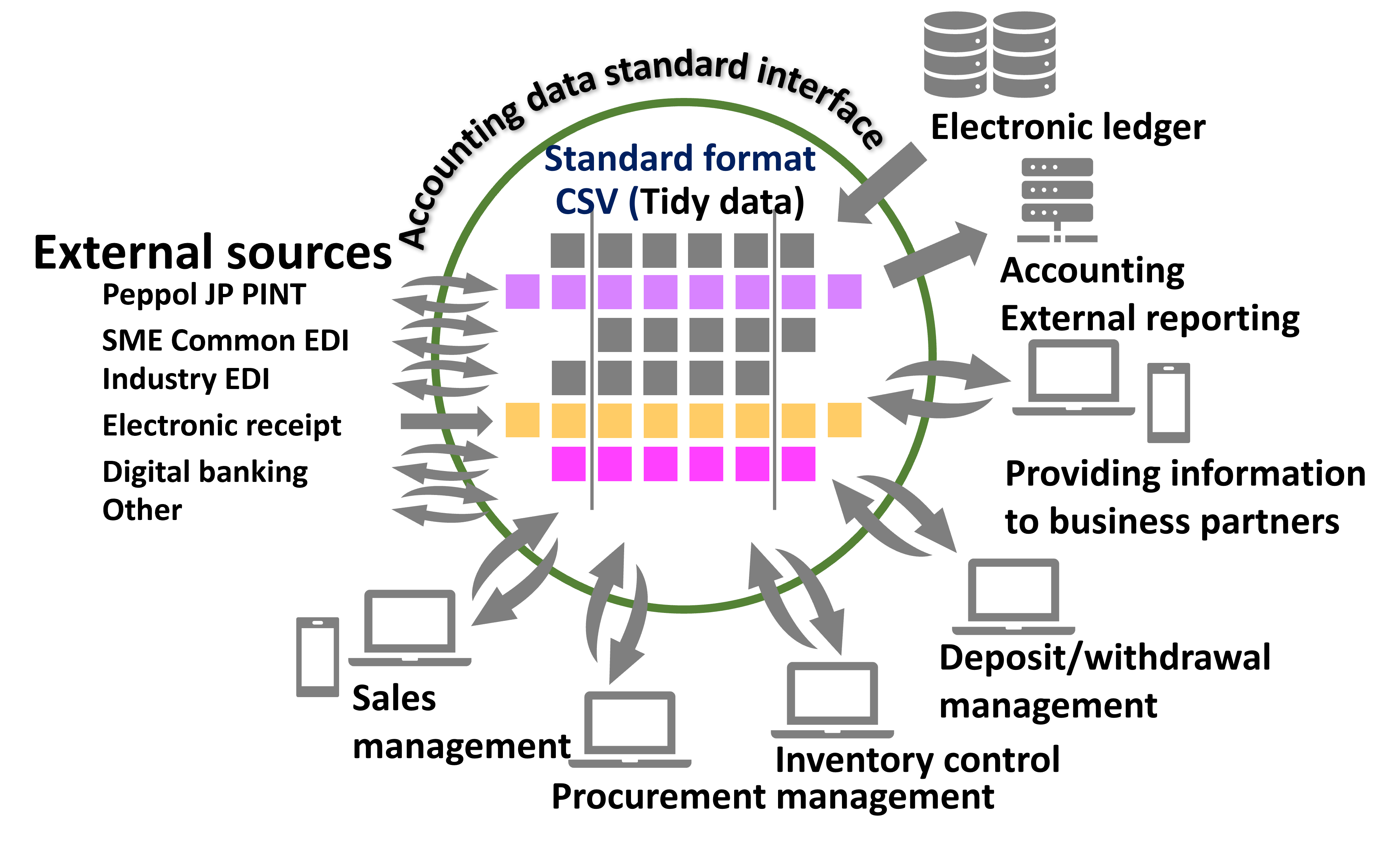

11. Accounting Data Standard Interface

Using a generic audit data converter enables the realization of an accounting data standard interface, as shown in the figure below. This system model is applicable for integrating information systems within individual companies (from an internal audit perspective) and centralizing information exchange with trading partners, as well as for accountants and tax advisors to grasp the foundational data of client organizations in real-time (from an external audit perspective).